Maryland business lawyer • LLC personal liability • piercing the corporate veil • asset protection • Rockville & Montgomery County

Does an LLC Protect My Personal Assets? Piercing the Corporate Veil in Maryland

Key Points

- An LLC generally protects your personal assets from the ordinary debts and lawsuits of the business, but the protection is not absolute.

- The most common way owners become personally liable is signing a personal guarantee, which is voluntary and enforced as written.

- You are always liable for wrongs you personally commit, and for certain taxes such as the trust fund portion of payroll taxes.

- Courts can pierce the corporate veil and reach owners personally, but both Maryland and Pennsylvania treat this as an extraordinary remedy.

- Maryland is one of the hardest states in which to pierce. Fraud is the clearest path, but a paramount equity can support piercing even without fraud. Pennsylvania uses a multi-factor test and does not require fraud as an absolute prerequisite.

- The shield stays strong when you treat the company as a truly separate business: separate accounts, adequate capital, contracts in the company name, and good standing with the state.

The short answer, and the important caveat

What an LLC does, and does not, do for you

For most business owners in Rockville, throughout Montgomery County, and across Maryland and Pennsylvania, forming a limited liability company is the single most important step they take to protect their personal savings, home, and other assets from the risks of the business. The premise is simple and, in the vast majority of cases, reliable: the LLC is a separate legal person, and its debts are its own, not yours.

But “generally protected” is not the same as “always protected.” The liability shield an LLC provides has real limits. Some owners sign the protection away without realizing it. Others lose it because a court decides the company was never truly operated as a separate business. And a handful of obligations, such as certain unpaid taxes and your own wrongful conduct, follow you personally no matter how the entity is structured.

This guide explains, in plain terms, how the LLC liability shield actually works under Maryland and Pennsylvania law, the specific situations where owners become personally liable anyway, and the legal doctrine courts use to reach through the entity, known as “piercing the corporate veil.” It also gives you a practical checklist for keeping your protection intact. If you are still deciding how to set up your company, start with our overview of business formation and structuring.

How limited liability actually works

The statutory shield in Maryland and Pennsylvania

When you form an LLC, the law treats the company as a distinct legal entity, separate from the people who own it. Owners of an LLC are called members. The central benefit of that separateness is limited liability.

Maryland says this directly. Under the Maryland Limited Liability Company Act, Section 4A-301 of the Corporations and Associations Article, a member is not personally liable for the debts, obligations, or liabilities of the LLC solely because the person is a member. The company can be sued, the company can owe money, and the company’s assets can be taken to satisfy its debts, but the members’ personal assets generally stay off limits. See Md. Code, Corporations and Associations, Section 4A-301.

Pennsylvania draws the same line. Under the Pennsylvania Uniform Limited Liability Company Act of 2016, 15 Pa.C.S. Section 8834, a debt, obligation, or other liability of an LLC is solely the debt of the company, and a member or manager is not personally liable simply by reason of being or acting as a member or manager. That protection applies whether the company has one member or many, and it continues even through the winding up and dissolution of the company.

This is the same protection a corporation gives its shareholders. Whether you operate as an LLC or a corporation, the entity stands between the business’s creditors and your personal bank account. For a closer look at how the two structures compare, see our guide on LLC vs. corporation. And for where to form, see our guides for Maryland owners and Pennsylvania owners deciding among their home state, Delaware, and Wyoming.

Why the shield is not absolute

Five situations where owners are personally liable anyway

Limited liability protects you from the ordinary debts and obligations of the business: a supplier invoice the company cannot pay, a commercial loan taken out in the company’s name, a slip and fall lawsuit against the business. It does not protect you from everything.

There are five recurring situations where owners of an otherwise valid LLC end up personally on the hook:

- You personally guaranteed the obligation.

- You committed the wrongful act yourself.

- The obligation is one the law imposes on you personally, such as certain unpaid payroll and trust fund taxes.

- A court pierces the corporate veil.

- You never properly formed or maintained the entity, or you let it lapse.

The rest of this guide walks through each of these, with the most common ones first. Understanding them is the difference between assuming you are protected and actually being protected.

Personal guarantees: the most common exposure

How owners voluntarily contract around their own protection

The single most common reason an LLC owner ends up personally liable has nothing to do with any exotic legal doctrine. It is a personal guarantee, and it is entirely voluntary.

A personal guarantee is a contract in which you promise to pay the company’s obligation out of your own pocket if the company does not. Banks routinely require personal guarantees before extending a business loan or line of credit to a small or closely held company. Commercial landlords frequently require them on a lease. Equipment lessors, franchisors, and key suppliers often ask for them as well. If you are signing a lease for space in Rockville or elsewhere, have it reviewed first: see our guide on commercial lease review in Maryland.

When you sign a personal guarantee, you are contracting around your own limited liability. The LLC shield does not fail. You have simply agreed, in a separate promise, to be personally responsible, and courts enforce that promise as written.

Your own wrongful acts always belong to you

Personal liability for your own torts, fraud, and signatures

An LLC protects you from liability that arises from the business. It does not give you a pass for wrongs you personally commit. This principle catches many owners by surprise.

If you personally act negligently and injure someone, defraud a customer, make a defamatory statement, or commit some other tort, you can be held personally liable for your own conduct, even though you were acting for the company. The company may also be liable, but the liability shield does not erase your personal responsibility for what you personally did. Professionals such as doctors, lawyers, accountants, and engineers remain personally responsible for their own malpractice regardless of the entity they practice through.

A related trap is signing in the wrong capacity. When you sign a contract on behalf of your LLC, you must sign as a representative of the company, showing the company name, your name, and your title, for example “ABC Ventures LLC, by Jane Doe, Managing Member.” If you sign a business contract in your own name without indicating that you are signing for the company, the other side may be able to hold you personally liable on the contract. This small habit matters more than most owners realize, and it is covered in our guide on contract mistakes to avoid.

Unpaid payroll and trust fund taxes

Why tax liability can bypass the LLC shield by law

Some tax obligations pierce the shield by operation of federal and state law, without any need to go to court. The most important one for employers is the trust fund portion of payroll taxes.

When a business withholds income tax and the employee’s share of Social Security and Medicare from employee wages, that money is held in trust for the government. If the business fails to pay it over, the Internal Revenue Service can assess the Trust Fund Recovery Penalty under Internal Revenue Code Section 6672 against any responsible person who willfully failed to collect or pay the tax. A responsible person can be an owner, officer, manager, or bookkeeper, essentially anyone with authority over the money and the decision of which bills to pay. The penalty equals 100 percent of the unpaid trust fund taxes, and it is a personal liability that the LLC shield does not stop.

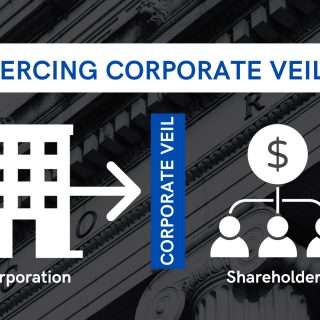

Piercing the corporate veil: what it means

The doctrine, who brings it, and what is at stake

“Piercing the corporate veil” is the legal doctrine that lets a court set aside the separateness of a business entity and hold its owners personally liable for the entity’s obligations. Although the phrase uses the word “corporate,” courts apply the same doctrine to LLCs. In Maryland, the appellate courts have said that piercing the veil of an LLC is treated much like piercing the veil of a corporation.

A veil-piercing claim usually arrives as part of a lawsuit by a creditor or plaintiff who has a claim against the business but suspects the business cannot pay, or who believes the owner has abused the entity. If the claim succeeds, the plaintiff can collect not only from the company but from the owner personally. These claims are litigated within the broader field of business disputes and litigation.

Both Maryland and Pennsylvania treat veil piercing as an extraordinary remedy. Courts in both states start from a strong presumption that the entity is separate and that the owners are not personally liable. The law protects the corporate and LLC form because limited liability encourages people to start businesses, take reasonable risks, and invest. Setting that protection aside is the exception, not the rule. But the standards, and how hard they are to meet, differ meaningfully between the two states.

Piercing the corporate veil in Maryland

Maryland’s fraud-centered standard and the leading cases

Maryland is widely regarded as one of the most difficult states in the country in which to pierce the corporate veil. The governing standard comes from the Supreme Court of Maryland, the state’s highest court, known until 2022 as the Court of Appeals of Maryland, in Bart Arconti & Sons, Inc. v. Ames-Ennis, Inc., 275 Md. 295 (1975): shareholders are generally not held individually liable for the debts or obligations of a corporation except where it is necessary to prevent fraud or enforce a paramount equity.

On its face, that standard offers two doors: fraud, or a “paramount equity.” Maryland courts have been extremely reluctant to find either sufficient, and historically most non-fraud veil-piercing arguments have failed. The Appellate Court of Maryland has repeatedly noted the absence of Maryland precedent actually piercing the veil on a paramount-equity theory alone. See Residential Warranty Corp. v. Bancroft Homes Greenspring Valley, Inc., 126 Md. App. 294 (1999), Ramlall v. MobilePro Corp., 202 Md. App. 20 (2011), and Serio v. Baystate Properties, LLC, 203 Md. App. 581 (2012). But in Schlossberg v. Bell Builders Remodeling, Inc., 109 A.3d 1146 (Md. 2015), the Supreme Court of Maryland confirmed that, where there is no allegation, evidence, or finding of fraud, the corporate veil may nonetheless be disregarded upon proof of a paramount equity. The state’s highest court has cautioned that the alter ego rationale supporting a paramount equity should be applied only with great caution and in exceptional circumstances. Hildreth v. Tidewater Equipment Co., 378 Md. 724 (2003). The practical point remains that Maryland courts apply the doctrine reluctantly, cautiously, and only in exceptional circumstances.

Where fraud is alleged, the party seeking to pierce must prove it by clear and convincing evidence, a demanding standard. Ordinary business failure, even insolvency, is not fraud.

The single-member LLC example: Serio v. Baystate Properties

A leading Maryland case shows how strong the protection is even for a one-owner company. In Serio v. Baystate Properties, LLC, 203 Md. App. 581 (2012), a builder was left unpaid after doing work connected to lots owned personally by the sole member of an LLC. The trial court pierced the LLC’s veil and held the member personally liable, reasoning that a paramount equity required it: the member owned the lots individually, the LLC was thinly funded and effectively insolvent, the member had made misleading statements about pending sales, and a promised escrow account was never set up.

The Maryland appellate court reversed. Because there was no finding of fraud, and because the builder had knowingly contracted with the LLC (the payments came from the LLC’s account, signed by the member as managing member, and the parties had even agreed the member would not be personally liable), the veil could not be pierced. The court also confirmed the statutory anchor: Section 4A-301 provides that no LLC member is personally liable for the LLC’s obligations solely by reason of being a member, and Maryland applies corporate veil-piercing principles to LLCs. The full opinion is available on Justia.

The lesson: a single-member LLC that is genuinely operated as a separate business can shield its owner in Maryland even when the company fails and cannot pay, so long as there is no fraud.

Piercing the corporate veil in Pennsylvania

Pennsylvania’s multi-factor test and the 2021 enterprise theory

Pennsylvania also begins with a strong presumption against piercing, but it gets there through a different, more flexible analysis. The Pennsylvania Supreme Court held in Lumax Industries, Inc. v. Aultman, 543 Pa. 38, 669 A.2d 893 (1995), that there is a strong presumption in Pennsylvania against piercing the corporate veil, and that a corporation is treated as an independent entity even if one person owns all of it. The full opinion is available on Justia.

When a Pennsylvania court does consider piercing, it weighs a set of factors drawn from Lumax:

- undercapitalization of the entity;

- failure to adhere to corporate formalities;

- substantial intermingling of corporate and personal affairs; and

- use of the corporate form to perpetrate a fraud.

No single factor is decisive. Unlike Maryland, Pennsylvania does not treat fraud as effectively mandatory. Fraud is one factor among several, and Pennsylvania courts have said the veil may be pierced, as a matter of equity, where one in control of the entity uses that control or the entity’s assets to further personal interests and injustice results. Even so, Pennsylvania calls veil piercing an extraordinary remedy reserved for exceptional circumstances. Village at Camelback Property Owners Ass’n v. Carr, 538 A.2d 528 (Pa. Super. 1988).

Pennsylvania law also contains an important protection for LLC owners specifically. Under 15 Pa.C.S. Section 8106, the failure of an LLC to observe formalities relating to the exercise of its powers or the management of its activities and affairs is not, by itself, a ground for imposing personal liability on a member or manager. In other words, an LLC is not expected to hold the same formal meetings and keep the same minute books a corporation does, and skipping those corporate style formalities alone will not sink the shield.

Pennsylvania’s veil-piercing law took a notable turn in 2021. In Mortimer v. McCool, 255 A.3d 261 (Pa. 2021), the Pennsylvania Supreme Court recognized the enterprise, or single entity, theory of liability, which can reach a sister company that shares common ownership and operates as part of a single business enterprise, rather than only reaching the individual owner. Pennsylvania is now among the minority of states to accept this theory. Importantly, the court declined to apply it on the facts before it, did not spell out a precise test, and went out of its way to reaffirm the strong presumption against piercing, emphasizing that great injustice and inequity must remain the touchstone. The practical effect: enterprise liability is now theoretically available in Pennsylvania, especially against owners who split a single business across multiple affiliated entities purely to dodge liability, but its boundaries remain unsettled.

Maryland vs. Pennsylvania at a glance

A side-by-side comparison of the two standards

The two states reach a similar destination, entities are respected and piercing is hard, but by different routes. This table summarizes the key differences.

| Issue | Maryland | Pennsylvania |

|---|---|---|

| Governing standard | Veil pierced only to prevent fraud or enforce a paramount equity (Bart Arconti) | Strong presumption against piercing; multi-factor alter ego analysis (Lumax) |

| Is fraud required? | Not formally, but fraud is the clearest and most commonly recognized path. A paramount equity can support piercing without fraud (Schlossberg), though Maryland courts rarely find one (Serio, Hildreth, Ramlall) | No. Fraud is one factor, not a requirement; piercing is available where the form is abused and injustice results |

| Core factors | Fraud, and alter ego or failure to observe the entity, applied with great caution | Undercapitalization, failure to follow formalities, intermingling of personal and company affairs, use of the form to commit fraud |

| Effect of ignoring formalities | Relevant to alter ego, but rarely enough by itself; fraud generally still needed | For LLCs, failure to observe formalities is not by itself a ground for liability (Section 8106) |

| Sister-company (enterprise) liability | Not recognized as a stand-alone path; the focus stays on fraud | Enterprise or single entity theory adopted in 2021 (Mortimer v. McCool), but not yet applied and the standard is unsettled |

| Overall difficulty | Among the most difficult states in which to pierce | Difficult; an extraordinary remedy for exceptional cases |

Factors and red flags courts look at

The fact patterns that draw scrutiny in both states

Whether a court is applying Maryland’s fraud-centered standard or Pennsylvania’s multi-factor test, the same fact patterns tend to draw scrutiny. The more of these that are present, the more exposed an owner becomes:

- Commingling of funds: paying personal expenses from the business account, or business expenses from a personal account, or moving money back and forth without documentation.

- Undercapitalization: starting or running the business with far too little money or insurance to meet its reasonably expected obligations.

- Ignoring the separateness of the entity: no separate bank account, no records, using company assets as if they were personal property.

- Failure to follow the entity’s own governance rules: for a corporation, skipping required meetings and minutes; for any entity, ignoring the operating agreement or bylaws. Remember that for Pennsylvania LLCs, this factor alone is limited by Section 8106.

- Domination and control used for personal ends: treating the company as a mere instrument for the owner’s personal dealings.

- Siphoning assets: draining money out of the business, especially as claims come due, leaving it unable to pay.

- Fraud or misrepresentation: using the entity to deceive creditors or to evade an existing legal obligation.

None of these guarantees a piercing, and in Maryland most of them will not be enough without fraud. But together they paint the picture courts look for: a business that was never really run as a business.

How to keep your liability shield intact

A practical checklist for owners

The good news is that keeping your protection is largely within your control. Treat the LLC as a genuine, separate business and the shield stays strong. A practical checklist:

- Keep separate bank accounts and credit cards for the business, and never pay personal expenses from them.

- Capitalize the business reasonably and carry appropriate insurance for its risks.

- Sign contracts in the company’s name, in your representative capacity, showing your title.

- Put “LLC” on your contracts, invoices, website, and signage so third parties know they are dealing with a company.

- Adopt and follow a written operating agreement, and document major decisions.

- Keep the business’s money in the business. Take money out through documented distributions, payroll, or reimbursements, not by dipping into the account.

- File your annual reports and keep the company in good standing with the state. In Maryland, an LLC that fails to file its annual report and business personal property return can forfeit its right to do business, which not only creates problems but undercuts the very separateness the shield depends on. See Maryland business not in good standing.

- When you close the business, dissolve and wind it up properly so that lingering obligations are handled and do not follow you. See how to close a business in Maryland.

For owners of LLCs and corporations who want a standing relationship to keep this maintenance on track, ongoing general counsel support and sound corporate governance can make the difference between a shield that holds and one that quietly erodes.

Single-member LLCs: extra caution

Why sole owners face closer scrutiny

Single-member LLCs get more scrutiny than multi-member ones, because the line between the owner and the company is easier to blur when there is only one person. Courts know that a sole owner can be tempted to treat the company account as a personal wallet. As Serio shows, a single-member LLC in Maryland can absolutely protect its owner, but the discipline has to be real: separate accounts, clean records, contracts in the company’s name, and no commingling. If you are the only member, the checklist above is not optional housekeeping. It is what preserves your protection.

Veil piercing vs. charging orders

A quick clarification of two things that are often confused

Veil piercing runs in one direction: a creditor of the business reaching the owner’s personal assets. The reverse situation, a personal creditor of the owner trying to reach the owner’s LLC, is handled very differently. In both Maryland and Pennsylvania, the usual starting point is a charging order, which is a lien on the member’s economic interest and requires the LLC to pay the creditor the distributions that otherwise would have gone to the debtor-member. Pennsylvania addresses charging orders in 15 Pa.C.S. Section 8853, and Maryland addresses them in Md. Code, Corporations and Associations, Section 4A-607.

A charging order generally does not give the creditor the company’s assets or ordinary management rights, but the remedy is not always limited to passively receiving distributions. Both states allow foreclosure on the charged interest in certain circumstances, typically where the creditor shows that distributions will not satisfy the debt within a reasonable time. Pennsylvania has a special rule for a sole member of an LLC: on foreclosure, the purchaser obtains the member’s entire interest and becomes a member, which can put the continued existence of a single-member LLC at risk. Under Maryland’s statute, the purchaser at a foreclosure sale takes the debtor’s economic interest as an assignee, meaning the purchaser can receive distributions but does not automatically obtain management rights or become a member. This is a distinct topic from veil piercing, but the two are frequently confused.

Does the same analysis apply to corporations?

How corporations and LLCs compare on veil piercing

Yes. The veil-piercing doctrine developed in the corporate context, and courts apply the same core principles to corporations and LLCs alike. The main practical difference is formalities. Corporations are expected to observe more of them, such as regular meetings, minutes, and resolutions, so a corporation that ignores those formalities may face more exposure on that factor than an LLC would. This is particularly true in Pennsylvania, where Section 8106 limits the significance of missed formalities for LLC owners. For a fuller comparison of the two structures and their tax treatment, see our guide on choosing between an LLC and a corporation.

How Iqbal Business Law can help

Iqbal Business Law helps business owners in Rockville, throughout Montgomery County, in Frederick, and across Maryland and Pennsylvania form and run their companies so that the liability protection they are counting on actually holds up. From our offices in Rockville and Frederick, we work with owners at every stage of the business.

We can help by:

- Forming your LLC or corporation and structuring it for genuine separateness

- Drafting operating agreements, bylaws, and governance procedures that support your liability shield

- Reviewing loans, leases, and vendor contracts to identify and negotiate personal guarantees before you sign

- Defending or asserting veil-piercing and related claims in business disputes

- Serving as outside general counsel to keep your entity compliant, in good standing, and protected over time

Related reads and resources

Official legal and government resources

- Md. Code, Corporations and Associations, Section 4A-301 (limited liability of LLC members)

- Md. Code, Corporations and Associations, Section 4A-607 (charging orders)

- Maryland State Department of Assessments and Taxation (SDAT)

- 15 Pa.C.S. Section 8834 (liability of LLC members and managers)

- 15 Pa.C.S. Section 8106 (failure to observe formalities)

- Pennsylvania Department of State: Limited Liability Companies

- Serio v. Baystate Properties, LLC (Maryland LLC veil-piercing decision)

- Schlossberg v. Bell Builders Remodeling, Inc., 109 A.3d 1146 (Md. 2015) (paramount equity without fraud)

- Lumax Industries, Inc. v. Aultman (Pennsylvania veil-piercing decision)

- IRS: Trust Fund Recovery Penalty

Related Iqbal Business Law insights

- Do You Need an LLC Operating Agreement in Maryland? What to Include and Why It Matters

- LLC vs. Corporation: Tax Implications and How to Choose the Right Structure for Your Business in 2026

- Should Maryland Small Businesses Form an LLC in Maryland, Delaware, or Wyoming?

- Should Pennsylvania Small Businesses Form an LLC in Pennsylvania, Delaware, or Wyoming?

- Maryland Business Not in Good Standing: How to Fix SDAT, Annual Report, and Forfeiture Problems

- How to Close a Business in Maryland: Dissolving Your LLC or Corporation

- Business Partner Dispute in Maryland: Your Legal Options

- IRS Trust Fund Recovery Penalty in Maryland and Pennsylvania

FAQ

Does an LLC protect my personal assets in Maryland?

Generally yes. Under the Maryland Limited Liability Company Act, Section 4A-301, a member is not personally liable for the debts or obligations of the LLC solely by reason of being a member, so your personal assets are usually protected from the company’s ordinary debts and lawsuits. That protection is not absolute. You can still be personally liable if you signed a personal guarantee, committed a wrongful act yourself, owe certain taxes such as trust fund payroll taxes, let the company lapse, or a court pierces the corporate veil.

Can I be sued personally if my business is an LLC?

Yes, in specific situations. An LLC shields you from the ordinary debts and obligations of the business, but a plaintiff or creditor can still reach you personally if you personally guaranteed the obligation, if you personally committed a tort or fraud, if the obligation is one the law imposes on you individually, or if a court agrees to pierce the corporate veil. Simply having an LLC does not, by itself, defeat every claim against you.

What does piercing the corporate veil mean?

Piercing the corporate veil is a doctrine that allows a court to disregard the separateness of a business entity and hold its owners personally liable for the entity’s obligations. Although the phrase says corporate, courts apply the same doctrine to LLCs. It is treated as an extraordinary remedy, and both Maryland and Pennsylvania start from a strong presumption that the entity is separate and the owners are not personally liable.

How hard is it to pierce the corporate veil in Maryland?

Very hard. Maryland is considered one of the most difficult states in which to pierce the veil. The standard from Bart Arconti and Sons, Inc. v. Ames-Ennis, Inc. allows piercing only to prevent fraud or enforce a paramount equity. Fraud remains the clearest and most commonly recognized path and must be proven by clear and convincing evidence, but in Schlossberg v. Bell Builders Remodeling, Inc. the Supreme Court of Maryland confirmed that a paramount equity can support piercing even without a finding of fraud. Maryland courts remain highly reluctant to find a paramount equity sufficient to pierce, and ordinary business failure or insolvency is not enough.

How is Pennsylvania different from Maryland on veil piercing?

Pennsylvania also applies a strong presumption against piercing, but it uses a more flexible multi-factor analysis rather than effectively requiring fraud. Under Lumax Industries, Inc. v. Aultman, courts weigh undercapitalization, failure to follow formalities, intermingling of personal and company affairs, and use of the entity to commit fraud. For LLCs, 15 Pa.C.S. Section 8106 provides that failing to observe formalities is not by itself a ground for liability. In 2021, in Mortimer v. McCool, the Pennsylvania Supreme Court also recognized an enterprise theory that can reach affiliated sister companies, though it did not apply the theory and its limits remain unsettled.

Does a single-member LLC protect my personal assets?

Yes, a single-member LLC can protect your personal assets, but it receives closer scrutiny because there is only one owner and the line between the person and the company is easier to blur. In the Maryland case Serio v. Baystate Properties, LLC, a single-member LLC’s shield held up even though the company failed and could not pay, because there was no fraud and the owner had genuinely operated it as a separate business. To keep the protection, a sole owner must maintain separate accounts, keep clean records, sign contracts in the company’s name, and avoid commingling funds.

Does a personal guarantee override my LLC’s liability protection?

In effect, yes. A personal guarantee is a separate contract in which you promise to pay the company’s obligation if the company does not. It does not defeat the LLC shield so much as contract around it. Banks, commercial landlords, equipment lessors, and some vendors commonly require personal guarantees from owners of small or closely held companies, and courts enforce them as written. Always check financing documents and leases for a guarantee, and negotiate its scope before signing.

Can I be personally liable for my LLC’s unpaid payroll taxes?

Yes. When a business withholds income and payroll taxes from employee wages, that money is held in trust for the government. If it is not paid over, the IRS can assess the Trust Fund Recovery Penalty under Internal Revenue Code Section 6672 against any responsible person who willfully failed to pay, including owners, officers, or anyone with authority over the funds. The penalty is a personal liability equal to the unpaid trust fund taxes, and the LLC does not shield you from it.

How do I keep my LLC’s liability protection intact?

Treat the LLC as a genuine, separate business. Keep separate bank accounts, capitalize the business reasonably and insure it, sign contracts in the company’s name and title, adopt and follow a written operating agreement, document major decisions, take money out only through proper distributions or payroll, and keep the company in good standing by filing required reports. In Maryland, letting the company fall out of good standing or forfeit its charter can undercut the separateness the shield depends on.

What is the difference between piercing the corporate veil and a charging order?

They run in opposite directions. Piercing the corporate veil is a business creditor reaching the owner’s personal assets. A charging order is the tool a personal creditor of the owner uses to reach the owner’s interest in the LLC. It is a lien on the member’s economic interest that requires the LLC to pay the creditor the distributions that would otherwise go to the debtor-member, and it generally does not give the creditor the company’s assets or management rights. But the remedy is not always limited to passively receiving distributions. Both Maryland and Pennsylvania allow foreclosure on the interest in certain circumstances, and Pennsylvania has a special rule for a sole member of an LLC under which the foreclosure purchaser becomes a member. Pennsylvania addresses charging orders in 15 Pa.C.S. Section 8853, and Maryland addresses them in Md. Code, Corporations and Associations, Section 4A-607.

Disclaimer: This post is for general informational and educational purposes only and does not constitute legal advice. The rules governing limited liability, personal guarantees, tax liability, and piercing the corporate veil are complex, differ between Maryland and Pennsylvania, and depend on the specific facts of each situation. Reading this post does not create an attorney-client relationship with Iqbal Business Law. For advice tailored to your business, consult a qualified Maryland or Pennsylvania business attorney.